Institutional Trading Report: Sanctions pressure and Red Sea insecurity keep markets on hold

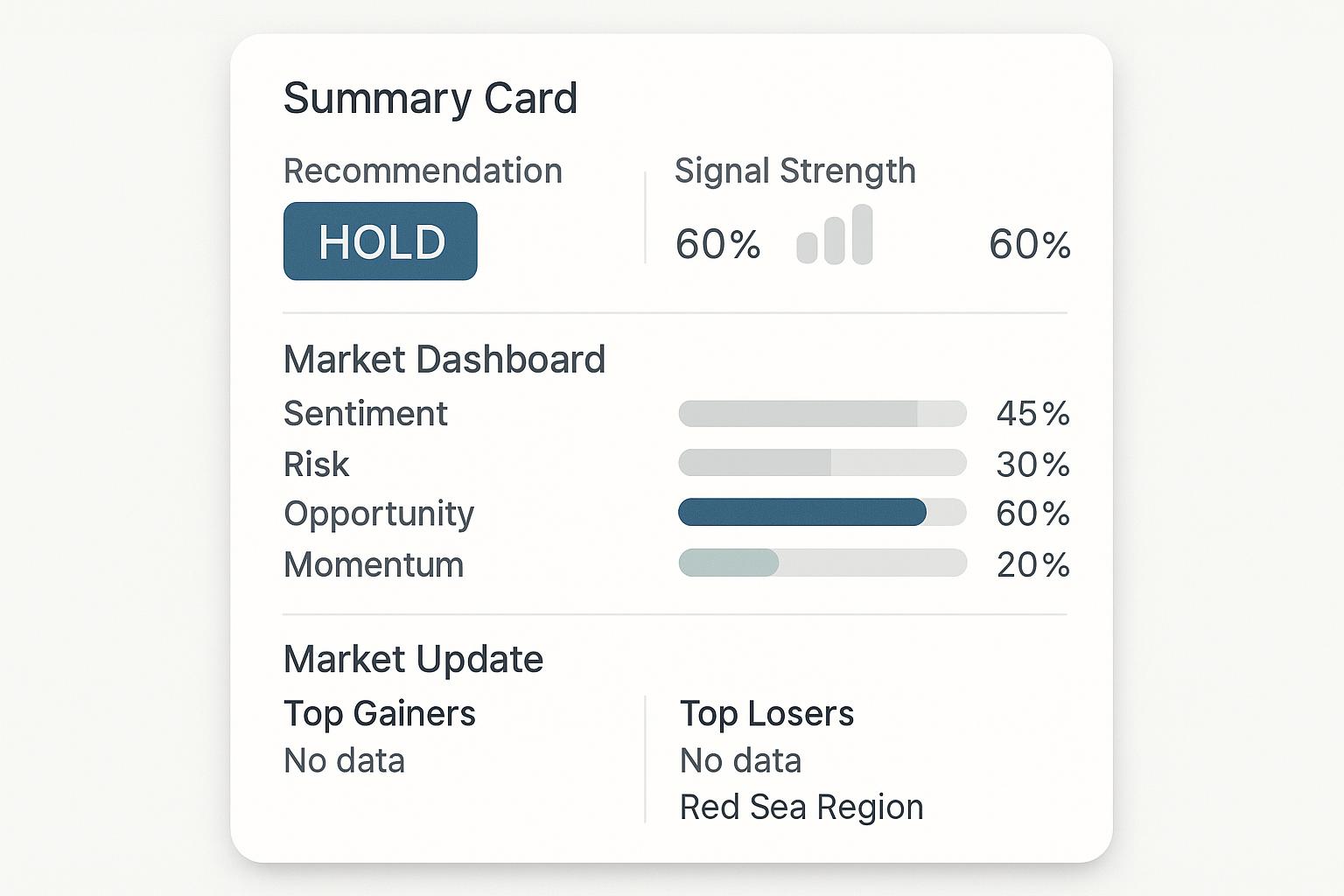

Executive Summary Key Takeaways • Aggregate sentiment is strongly negative (internal score -7.29) with moderate measured risk (45.6/100). • Opportunity is weak (21.0/100) while momentum is sharply negative (-1.0), producing a downward directional bias. • Volatility is elevated (normalised to 1.0) and confidence is moderate (0.60) based on 320 evidence items. • Rising thematic attention is concentrated on sanctions/shadow-fleet, Red Sea security and reopening, port fees/trade policy, LNG/bunkering and shipbuilding; AI in logistics is emergent. • The model therefore issues a mid-strength 'hold' recommendation (≈48/100), flagging close monitoring rather than immediate de-risking or aggressive repositioning.

Full Explainer Across the dataset, the integrated signal set points to a deeply negative tone, with overall sentiment at -7.29 on the internal scale, moderate aggregate risk at 45.6/100, and weak opportunity at 21.0/100. Momentum is strongly negative (-1.0), indicating a clear downward directional bias in forward-looking signals, while volatility is elevated (normalised to 1.0), tempering conviction despite a moderate confidence score of 0.60 supported by 320 evidence items.

Forward signals are most concentrated in themes around freight-rate and sanctions dynamics, security on key trade lanes, and evolving regulatory frameworks. Rising momentum is strongest in 'sanctions_and_shadow_fleet', 'shipbuilding_and_orderbook', 'LNG_market_and_bunkering', 'port_fees_and_trade_policy', 'Red_Sea_security_and_reopening' and emerging 'AI_in_logistics_and_chartering', while 'geopolitical_risk', 'port_congestion_and_performance', 'decarbonisation_and_IMO' and 'maritime_security_and_piracy' remain structurally important but directionally stable. On the entity side, attention is rising around 'China', 'Russia', 'Houthi / Red Sea', 'Tankers / VLCC' and 'LNG / LNG carriers', with the 'United States', the 'Red Sea / Suez Canal' corridor and 'Container carriers' providing a stable baseline of reference.

Because negative sentiment and falling momentum are not paired with extreme risk scores or very low confidence, the model’s trading logic resolves to a 'hold' signal with moderate strength (c.48 on a 0–100 scale). In other words, the forward indicators highlight a deteriorating but still manageable environment in which existing exposures are flagged for close monitoring rather than immediate de-risking or aggressive repositioning.

The market tone embedded in the dataset is distinctly risk-averse. The aggregate sentiment score of -7.29 is strongly negative, yet it co-exists with only mid-range quantified risk at 45.6/100 and a normalised volatility reading of 1.0, signalling a fragmented and unsettled backdrop. The moderate confidence score of 0.60, built on 320 evidence items, indicates that while the signal is statistically well supported, dispersion across inputs prevents a higher conviction rating.

Momentum is uniformly negative, with the composite momentum metric at -1.0 and an 'overall_direction' of 'falling'. The small but positive acceleration_rate of 0.0167, combined with period-over-period changes of 0, -36, -0.05 and -0.1, suggests an initial sharp deterioration followed by a sequence of smaller incremental declines rather than a stabilising rebound. The identified 'period_3_4_opportunity_inflection' points to a short-lived improvement in opportunity that was insufficient to reverse the prevailing downtrend.

Regulatory forces are a central part of this context. The strongest mapped pressures arise from 'US_port_fees' and 'China_port_fees', reinforced by 'EU_sanctions_on_Russia'. Structural climate and trade policy drivers such as 'IMO_net_zero' and 'EU_CBAM' are present but lower-intensity, indicating that decarbonisation and border-adjustment regimes are shaping the background operating environment rather than acting as the dominant near-term shock.

On the structural side, supply-chain stresses are concentrated in 'rerouting_and_longer_voyages' and 'port_capacity_and_congestion', with additional sensitivity to 'blank_sailings_and_capacity_management' and 'nearshoring_and_trade_lane_shift'. Demand-side and macro factors, 'tariffs_and_trade_policy', 'energy_market_shifts' and 'global_demand_weakness', underline that the signal set is not purely operational, but also reflects softer underlying trade and energy conditions. Defence-related factors, captured through 'naval_deployments_and_responses' and 'piracy_and_private_security', are present at lower intensity but interact with maritime security themes.

Rising themes provide the clearest forward signals in the dataset. 'sanctions_and_shadow_fleet' and 'shipbuilding_and_orderbook' show both high thematic weight and rising momentum, indicating sustained attention on how sanctions enforcement and fleet composition may reshape future trade patterns and capacity. 'LNG_market_and_bunkering', 'port_fees_and_trade_policy' and 'Red_Sea_security_and_reopening' also register as rising, pointing to a growing focus on fuel dynamics, cost pass-through mechanisms and the security and reopening trajectory of a key chokepoint. 'AI_in_logistics_and_chartering' is smaller in absolute weight but stands out as an emergent efficiency and compliance theme.

In contrast, no themes are explicitly classified as falling; instead, several structurally important topics remain directionally stable. 'geopolitical_risk', 'port_congestion_and_performance', 'decarbonisation_and_IMO' and 'maritime_security_and_piracy' continue to carry significant weight without a clear acceleration either higher or lower, suggesting that they are now embedded as baseline conditions rather than incremental shock drivers. Unclassified themes such as 'freight_rate_volatility' and 'container_rate_decline_and_oversupply' likewise appear as persistent concerns rather than areas where sentiment is clearly improving or deteriorating on the latest readings.

Multi-period dynamics reinforce this picture. The large negative shift early in the period and subsequent smaller declines, together with the falling overall_direction, indicate that the main adjustment in expectations has already occurred and is now being refined at the margin. The momentum_ladder places rising sanctions-, security- and trade-policy-related themes at the top, followed by a dense cluster of stable but high-weight topics such as 'freight_rate_volatility', 'geopolitical_risk' and 'port_congestion_and_performance'. The absence of clearly falling themes means that, for now, the dataset points to a repricing around entrenched risks and constraints rather than to a broad-based normalisation.

Risk exposure in this signal set is concentrated in three composite categories: 'geopolitical_and_route_disruption_risk' (22.85), 'sanctions_enforcement_and_shadow_fleet_risk' (21.63) and 'market_oversupply_and_freight_decline_risk' (21.05). These are complemented by material but secondary contributions from 'regulatory_fragmentation_and_trade_policy_risk' (14.24) and 'operational_port_disruption_and_congestion_risk' (13.40), with 'piracy_and_local_security_risk' forming a smaller but non-negligible tail. The pattern indicates that route stability, sanctions compliance and demand–supply balance in freight markets are the key forward-looking vulnerabilities.

Upside potential is more selective and tends to sit in adaptation themes rather than in broad cyclic strength. Rising attention around 'LNG_market_and_bunkering' and 'shipbuilding_and_orderbook' suggests that opportunities cluster in areas that can benefit from changes in fuel usage, fleet renewal and evolving trade lanes. At the margin, 'AI_in_logistics_and_chartering' and 'AI_for_sanctions_detection' point to efficiency and compliance technologies as niche areas of potential upside within an otherwise cautious backdrop.

Vulnerabilities arise where negative overall momentum intersects with high-risk categories. The combination of falling aggregate momentum, weak opportunity (21.0/100) and elevated 'market_oversupply_and_freight_decline_risk' underscores sensitivity in segments exposed to excess capacity and softer freight demand, including themes such as 'freight_rate_volatility' and 'container_rate_decline_and_oversupply'. Similarly, the pairing of 'sanctions_enforcement_and_shadow_fleet_risk' with rising 'sanctions_and_shadow_fleet' attention highlights potential pressure points for actors reliant on opaque or high-risk routing and ownership structures.

Operationally, the supply_chain_map shows that 'rerouting_and_longer_voyages' and 'port_capacity_and_congestion' are the dominant sensitivities, amplified by 'blank_sailings_and_capacity_management', 'nearshoring_and_trade_lane_shift', 'inventory_and_frontloading' and pockets of 'US_imports_and_domestic_freight_contraction'. These are overlaid by defence- and security-related factors such as 'naval_deployments_and_responses' and 'piracy_and_private_security', particularly around the 'Red Sea / Suez Canal' and 'Somalia / Indian Ocean' regions, where security-driven disruptions can compound existing logistical and regulatory stresses.

From a strategic standpoint, the strong negative momentum and low opportunity score argue against aggressively increasing exposure to the broad complex, yet the pattern of rising themes points to where relative resilience and future optionality may lie. Within the model, areas linked to 'LNG_market_and_bunkering', 'shipbuilding_and_orderbook' and 'AI_in_logistics_and_chartering' combine rising thematic momentum with comparatively constructive forward narratives, supporting a relative overweight stance in adaptation- and efficiency-focused segments, subject to idiosyncratic risk assessment.

Conversely, themes associated with high composite risk and entrenched negative tone are candidates for relative underweight. The prominence of 'sanctions_and_shadow_fleet', together with 'sanctions_enforcement_and_shadow_fleet_risk', points to elevated enforcement and compliance uncertainty, while 'market_oversupply_and_freight_decline_risk' and 'freight_rate_volatility' flag structural pressure in oversupplied freight segments. In combination with stable but sizeable 'geopolitical_risk' and 'port_congestion_and_performance' signals, this tilts the model away from highly leveraged exposure to the most disruption-prone routes and asset classes.

Time-horizon sensitivity is shaped by the modest acceleration_rate (0.0167) and the recency-weighted construction of the signal set, which together indicate that conditions are deteriorating but not yet in a phase of rapid regime change; the signals are therefore most informative for near- to medium-term positioning and risk budgeting rather than for very long-term structural calls. Policy and regulatory drivers, 'US_port_fees', 'China_port_fees', 'EU_sanctions_on_Russia', 'IMO_net_zero' and 'EU_CBAM', and structural bottlenecks in 'rerouting_and_longer_voyages' and 'port_capacity_and_congestion' should be treated as persistent constraints around which strategy is optimised, rather than transient factors likely to dissipate quickly.

Market Context • The dataset reflects a risk-averse market: strong negative sentiment (-7.29) co-existing with mid-range quantified risk (45.6/100) and normalised high volatility (1.0). • Momentum is uniformly negative (composite -1.0; overall_direction: falling) with a modest positive acceleration_rate (0.0167) and a multi-period pattern of a sharp initial deterioration followed by incremental declines. • Regulatory and policy pressures are prominent: US and China port fees and EU sanctions on Russia are meaningful near-term drivers; IMO and CBAM remain background structural influences. • Supply-chain stress is concentrated in rerouting and longer voyages and port capacity/congestion, amplified by blank sailings and nearshoring shifts. • Geographic intensity is highest for the United States and China/South China Sea, with the Red Sea/Suez corridor and Europe also materially active.

The market tone embedded in the dataset is distinctly risk-averse, with negative sentiment, falling momentum and elevated volatility.

Recent policy actions and industry analysis underline the interaction between sanctions and route choices: Western measures against Russian energy firms have forced Lukoil's trading arm into wind-down, while the Suez Canal Authority and IMO are working to encourage a gradual return of traffic as security stabilises. At the same time, Sea-Intelligence estimates that re-routing via the Cape is currently tying up around 2.1m TEU of capacity – about 6.5% of the global fleet – implying that any durable Red Sea re-opening would materially reshape effective supply and port workloads.

Trend Analysis • Rising themes: sanctions_and_shadow_fleet, shipbuilding_and_orderbook, LNG_market_and_bunkering, port_fees_and_trade_policy, Red_Sea_security_and_reopening and AI_in_logistics_and_chartering. • No explicit falling themes were identified; several high-weight topics remain directionally stable (geopolitical_risk, port_congestion_and_performance, decarbonisation_and_IMO, maritime_security_and_piracy). • Momentum ladder places sanctions and shipbuilding at the top, followed by LNG, port-fees and Red Sea reopening; freight-rate_volatility remains a persistent concern. • Multi-period dynamics show a large early-period decline followed by smaller degradations; the main repricing has occurred and further changes are marginal.

Forward-looking momentum is concentrated in sanctions/shadow-fleet and Red Sea/security-related themes, while several core risk topics remain stable; overall momentum is falling.

Exposure Assessment • Principal exposure concentrations are geopolitical_and_route_disruption_risk (22.85), sanctions_enforcement_and_shadow_fleet_risk (21.63) and market_oversupply_and_freight_decline_risk (21.05). • Upside is selective: adaptation themes (LNG/bunkering, shipbuilding/orderbook) and efficiency/compliance tech (AI_in_logistics_and_chartering, AI_for_sanctions_detection) show limited opportunity. • Vulnerabilities are highest where falling momentum intersects with oversupply and freight-rate pressure (container_rate_decline_and_oversupply, freight_rate_volatility). • Operational sensitivities cluster on rerouting_and_longer_voyages and port_capacity_and_congestion, which are amplified by security-driven disruptions in the Red Sea/Suez and Somalia/Indian Ocean corridors.

Risk exposure is concentrated in three composite categories, route disruption, sanctions/shadow-fleet enforcement, and market oversupply/freight decline, while opportunities are narrow and adaptation-focused.

Strategic Implications • Given strong negative momentum and weak opportunity, avoid broad increases in exposure; favour monitoring and selective allocation adjustments rather than aggressive reweighting. • Relative overweight potential sits with adaptation and resilience themes (LNG_market_and_bunkering, shipbuilding_and_orderbook, AI_in_logistics_and_chartering) after idiosyncratic risk checks. • Relative underweight candidates include disruption-prone, oversupplied freight segments and entities heavily exposed to sanctions/opaque ownership structures. • Time-horizon sensitivity: signals are most informative for near- to medium-term positioning due to modest acceleration and recency-weighted construction. • Persistent policy/regulatory drivers and structural bottlenecks should be treated as constraints around which strategies are optimised.

Adopt a cautious, monitoring-first stance; favour targeted overweight in adaptation/efficiency themes and relative underweight for disruption- and oversupply-prone exposures, focusing on near- to medium-term positioning.

Core Analytics

| Signal | Score | Range | Interpretation |

|---|---|---|---|

| Sentiment | -7.29 | -1 to 1 | Negative |

| Risk | 45.6 | 0-100 | Moderate |

| Opportunity | 21.0 | 0-100 | Weak |

| Momentum | -1.0 | -1 to +1 | Decelerating |

| Volatility | 1.0 | 0-1 | High |

| Rank | Theme | Momentum | Direction | Change |

|---|---|---|---|---|

| 1 | sanctions_and_shadow_fleet | 1.0 | ↑↑ | n/a |

| 2 | shipbuilding_and_orderbook | 1.0 | ↑↑ | n/a |

| 3 | LNG_market_and_bunkering | 1.0 | ↑↑ | n/a |

| 4 | port_fees_and_trade_policy | 1.0 | ↑↑ | n/a |

| 5 | Red_Sea_security_and_reopening | 1.0 | ↑↑ | n/a |

| 6 | AI_in_logistics_and_chartering | 1.0 | ↑↑ | n/a |

| 7 | freight_rate_volatility | 0.0 | → | n/a |

| 8 | geopolitical_risk | 0.0 | → | n/a |

| 9 | port_congestion_and_performance | 0.0 | → | n/a |

| 10 | maritime_security_and_piracy | 0.0 | → | n/a |

| 11 | decarbonisation_and_IMO | 0.0 | → | n/a |

| 12 | container_rate_decline_and_oversupply | 0.0 | → | n/a |

| 13 | AI_for_sanctions_detection | 0.0 | → | n/a |

Entity Performance

| Entity | Sentiment | Trend |

|---|---|---|

| China | Positive | Rising |

| Russia | Positive | Rising |

| Houthi / Red Sea | Positive | Rising |

| Tankers / VLCC | Positive | Rising |

Theme Movement

| Theme | Current Weight | Prior Weight | Delta | Interpretation |

|---|---|---|---|---|

| sanctions_and_shadow_fleet | 13.33 | n/a | n/a | Accelerating |

| shipbuilding_and_orderbook | 12.85 | n/a | n/a | Accelerating |

| LNG_market_and_bunkering | 7.89 | n/a | n/a | Accelerating |

| port_fees_and_trade_policy | 7.18 | n/a | n/a | Accelerating |

| Red_Sea_security_and_reopening | 7.10 | n/a | n/a | Accelerating |

| AI_in_logistics_and_chartering | 0.93 | n/a | n/a | Accelerating |

| Theme | Current Weight | Prior Weight | Delta | Interpretation |

Geographic Distribution

| Region | Activity | Sentiment | Risk Level |

|---|---|---|---|

| United States | High (7.44) | n/a | n/a |

| China / South China Sea | High (6.20) | n/a | n/a |

| Red Sea / Suez Canal | Medium (5.42) | n/a | n/a |

| Europe / EU | Medium (4.65) | n/a | n/a |

| India / Asia | Low (3.72) | n/a | n/a |

| Somalia / Indian Ocean | Low (1.24) | n/a | n/a |

Trading Signal Breakdown

| Signal Component | Value | Weight | Contribution |

|---|---|---|---|

| Sentiment | Negative | 30% | n/a |

| Momentum | Strong negative | 25% | n/a |

| Risk-Adjusted | Moderately unfavourable | 45% | n/a |

| TOTAL | hold | 100% | n/a |

External Context These external findings support maintaining a cautious 'hold' stance, as they validate the prominence of sanctions, Red Sea security and freight-rate volatility already embedded in the internal signal set. They do not provide a sufficiently clear or one-sided near-term price trend in the key entities to justify upgrading the recommendation to a more directional 'buy' or 'sell' call.

Report Generated: 2025-11-21 Noah Wire Services